Home

Latest updates & news

About Us

About Company and Services

Blogs & Insights

Latest updates & news

Customer Reviews

Need Help?

Call Us

+65 3129 4104

Operating Hours

Mon-Sun: 8AM-10PM

Written by

Many people borrow money from the lender, but they cannot pay it back to the creditor even after many requests. If this happens with you, you can file a bankruptcy application in Singapore against your debtor.

If the application gets approved by the high court, the debtor will be considered bankrupt. If you’re also one of those creditors willing to file a bankruptcy application against the debtor who cannot pay your borrowed money. Then continue reading the guide here we have explained step by step process on how you can file a bankruptcy application in Singapore against the debtor.

Besides this, if you are willing to set up an offshore company in Singapore but not getting the relevant guide, then you must check our setting up offshore company guide.

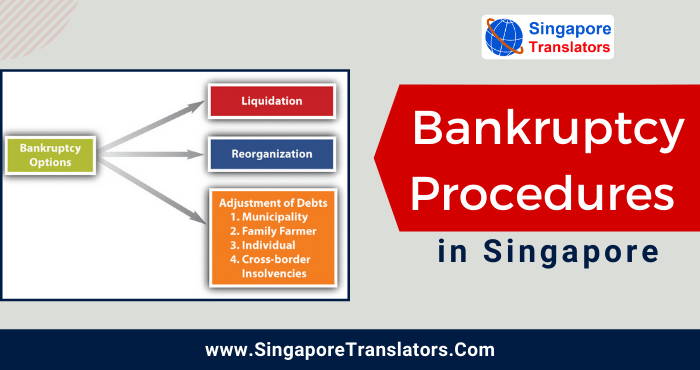

Bankruptcy is defined as the legal process managed by the court to help those individual and business entities who are struggling to pay off the debt to the creditors using the assets or property they owe.

There are six steps involved in filing the bankruptcy application in Singapore:

Step 1

You will require receiving and filing the following relevant form for:

Step 2

In the Next step, you will require to pay the bankruptcy amount of $1850 with the official assignee (OA). You can pay the bankruptcy deposit via cash by visiting Sing Post counters, and a payment receipt will be provided. (Note: Keep that payment receipt with you for future reasons).

On the other side, you also have the option to pay the bankruptcy deposit using Pay Now. You will be required to send an email to Min Law’s Finance Department at finance@mlaw.gov.sg for requesting Pay Now Proxy and Payment instructions. Once the payment has been processed, you will receive the payment receipt through email within four working days.

Step3

Carry all the completed documents.

In the Next step, you will be required to bring the completed document (given in Step 1 and the payment receipt that you received while paying the bankruptcy deposit) to the Supreme Court legal registry situated at level 2 of Supreme Court, and then you will require to release the payment for the prescribed stamp/Commissioner for Oaths fees.

Step 4

No, you will require to move forward to proclaim the Affidavit Verifying Statement of Affairs and affidavit in support of Debtors bankruptcy application prior to visiting commissioner for Oaths, which is situated at a level 3M of the Supreme Court Commissioner for oaths will stamp and sign on the completed documents which ensure that the documents are verified.

Step 5

After receiving a stamp and signature from the Commissioner oath, you will require to visit the Lawnet Service Bureau, situated at level 1of the Supreme Court, to submit all the documents through litigation only after you have paid the required fees. The Lawnet Service Bureau will update you regarding the date when you can collect your documents. The time and date regarding the bankruptcy hearing will also be mentioned on the application.

Step 6

You need to attend the hearing on the given date and time on the application. If not, you will require to send a written application to the registrar of the Supreme Court to request for extending the hearing date mentioning the reason for extending.

Points to remember: Excluding For statement of affairs (which needs to be handwritten), all other required forms need to be typed. You do not need to sign an Affidavit in Support of Debtor’s Bankruptcy Application and the Affidavit Verifying Statement of Affairs form as it stamps and signature needs to be done by Supreme Court commissioner for oaths.

A creditor can only file the bankruptcy application against you if you do not satisfy statutory demand, i.e., if you do not make the debt payment on time. No matter whosoever files the bankruptcy application, Debtor or the creditor, the bankruptcy order will always be made by the High Court only if the application gets approved.

Debtor themselves or a creditor can only file the bankruptcy application to declare the debtor as bankrupt if a debtor comes under the following situations:

If the Debtor owes the minimum amount of $15,000, where the debt is easily payable quickly and enforceable in Singapore, debtors cannot pay the debt.

Suppose a creditor files the bankruptcy application. In that case, the debtor will only be considered as being unable to pay the debt if any of the following situations are met:

There are few situations given below under which you must file bankruptcy:

In such a situation, filing a bankruptcy is one of the ideal options as:

1. Your debt stops accumulating

Once a bankruptcy request has been filed against the debtor (order will be issued by the high court claiming debtor as bankrupt), the creditors are not allowed to charge any interest on the outstanding sum owed. Thus, the debt owed is frozen at a certain amount.

2. Your monthly repayments are lower

Earlier, your creditor might be running behind you for receiving monthly repayments which were out of your means. But once you are declared bankrupt, all the repayments will be managed by the official assignee. They will tell you the decision regarding the required amount of money contribution that you will need to pay after considering you and your family’s needs.

This means that the monthly contribution amount decided by the official assignee will be far more reasonable and will be within your means as compared to the earlier when your creditors were running behind you every month to receive the payments.

3. Creditors are not permitted to sue you for debts

Creditors are restricted from performing any legal proceedings against you to receive the repayments of the debt prior to bankruptcy or after making the bankruptcy request.

Note: In order to get transcription service for court proceedings you can choose our experienced translator from Singapore translators.

If a foreigner wanted to open a bank account in Singapore, then surely you can open but you need some extra documents and have to fulfil some formalities which are given in this guide Expat Or A Foreigner To Open Bank Account In Singapore.

Debtors can proceed with filing bankruptcy requests in Singapore if they feel that they cannot repay the debts of a minimum of S$15,000. On the other hand, a creditor of the debtor can also have the option to file bankruptcy in order to make the debtor go bankrupt if they feel that the debtor cannot pay the owed debts.

If the debtor is considered bankrupt after filing a bankruptcy request, then all their assets will be sold and sent to the bankruptcy estate. However, some of the protected assets from bankruptcy will not be sold or sent to bankrupt assets like HDB flats.

Your assets that will be sent to bankruptcy estate will be handled by the official assignee (OA). As the functioning of the debtor’s bankruptcy estate is usually managed by an official assignee (OA). The official assignee (OA) is an officer appointed by the court to handle all the debtors’ assets and disseminate them among the creditors. On the other side, the bankruptcy estate can also be handled by a private trustee who can either be an accountant or lawyer.

Those who are declared bankrupt but gainfully employed in any profession need to make a monthly contribution which is paid to the bankruptcy estate. The fulfilling a target of monthly contribution will be decided by the official assignee or accountant, or lawyer who is managing the bankruptcy estate. Those properties or assets that are already in bankruptcy estate cannot be used to pay off the monthly target contribution.

Once the target contribution set by the official assignee (OA) is paid off, the bankrupt will be released from bankruptcy.

Certified translations for ICA, MOM, MFA and all government agencies

It will be much beneficial for you to self declare yourself bankrupt rather than remain to wait for the creditor to do so. This is because if you keep waiting for a creditor to sue you, the interest of the owed amount will keep on increasing as time passes.

However, irrespective of who filed the request for bankruptcy, the cost of the bankruptcy application will be ensured by the debtor.

ICA-certified translators for document, legal, and certified translations

Any creditor or debtor who filed the bankruptcy application needs to pay the deposit of $1850 to the official assignee (OA) who will manage the debtor’s bankruptcy estate as explained above.

For the approved bankruptcy application filed by the creditor, the creditor can recover the complete amount of the bankruptcy application deposit if there are any additional funds in the debtor bankrupt estate. Moreover, if the application filed by the debtor is successfully approved, the deposit of $1850 will not be refunded.

In case the bankruptcy application has been rejected, the official assignee (OA) will return the $1800 to the applicant (be it debtor or creditor). But the remaining $50 will be kept as preliminary administration cost.

If you appoint a lawyer in order to guide you to file a bankruptcy application, then the professional fees of the lawyer will be on top of the bankruptcy deposit amount.

After 21 days of bankruptcy request, you will need to visit the official assignee’s (OA) office to get complete details regarding your responsibilities as bankrupt. You will also be required to submit a Statement of Affairs form giving information about your assets and liabilities to OA.

After that, you must also start discussing the monthly target contribution plan with OA.

Here are some of the roles of the official assignee (OA):

After you are declared bankrupt, all your assets will be sent to the bankruptcy estate and will be handled by the official assignee appointed by the High Court. Those creditors who have shown the proof to the OA regarding the debt provided to the debtor get liable to obtain the dividends from the debtor‘s bankruptcy estate.

Those assets that can become part of your bankruptcy estate are given as follows:

Any profit received from the sale of the assets will also be added to the bankruptcy estate, excluding the value of those assets which are secured debt.

Moreover, also various assets can be termed as a protected asset and will not be included in the bankruptcy Estate and hence it cannot be distributed among the creditors. Some of them include:

HDB flat only if at least one flat owner is a Singapore citizen

Money is in the CPF account.

A life insurance policy has taken on express trust for the spouse and children

Any personal equipment or items which can be used in your employment, vocation, or business

That equipment or furniture which is needed for your family

The leftover money of your monthly income is received after getting deducted from the monthly target contribution.

Any annual wage or bonus supplement which was paid to you as a part of your monthly income will also be excluded from the bankruptcy estate.

All those assets were previously given to the creditor in order to secure the loans, and now it does not belong to the secured assets. Creditors can sell those assets if you are not paying monthly contributions timely.

Your name will go into the bankruptcy register.

Once you are considered bankrupt, your name will be added to the bankruptcy register with the list of bankruptcies in Singapore. Anyone can check the list of bankruptcies in Singapore, not just the employer but also the general public, by paying the required fee.

However, based on how you are getting yourself discharged from bankruptcy, getting your name out of the bankruptcy register after a specific period of time is possible. As soon as you pay off all the outstanding debt amount of the creditor, you will be discharged from bankruptcy.

Will your family have to help repay your debts?

Only under one condition, your family can contribute to repaying the debt if they are co-borrowers of the debt along with you. Some of its examples are as follows:

If you and your spouse are currently residing in any of the HDB flats, then it’s your responsibility to update HDB regarding your current financial situation so that HDB cannot take any legal action against you for any of the due payments. Moreover, HDB can also help you out during difficult times to expedite your present financial condition.

Will you be able to work?

Yes, you will be granted to keep working as usual even after you are declared bankrupt.

Are you able to undergo divorce proceedings?

Yes, even after getting declared bankrupt, you can still file the request for divorce with your spouse. In addition, if your spouse is not comfortable with you because of your bankrupt status, they can also request for divorce against you.

After you are considered bankrupt, you will have to take some of the responsibilities. Some of them are as:

Besides this, several other restrictions will be imposed on you who you need to follow.

We hope the above guide has helped you in understanding everything about bankruptcy procedures in Singapore.

In addition to this, if you are willing to get assisted by a reliable document translation agency in Singapore to offer you translation service in Singapore, then a Singapore translator has got you covered. We have a team of the highly experienced translator that believes in delivering the efficient document translation at a low-cost.

Our team has been helping people in Singapore with document translation since 2003. We work with certificates, legal papers, ICA documents, and more. Every blog you read here is written by our in-house experts who handle these documents every single day. We share simple, useful guides to help you make the right choices.

View all posts by Singapore TranslatorsMore insights from our translation experts

Singapore Company Law provides a number of benefits to foreign entrepreneurs interested in establishing a…

As everyone knows that Singapore is considered one of the most preferred destinations in Asia,…

The intellectual property protection act in Singapore provide security to all types of intellectual work…